Phenom 100, Phenom 300, Citation CJ2, Citation CJ3, Citation CJ4, Citation M2

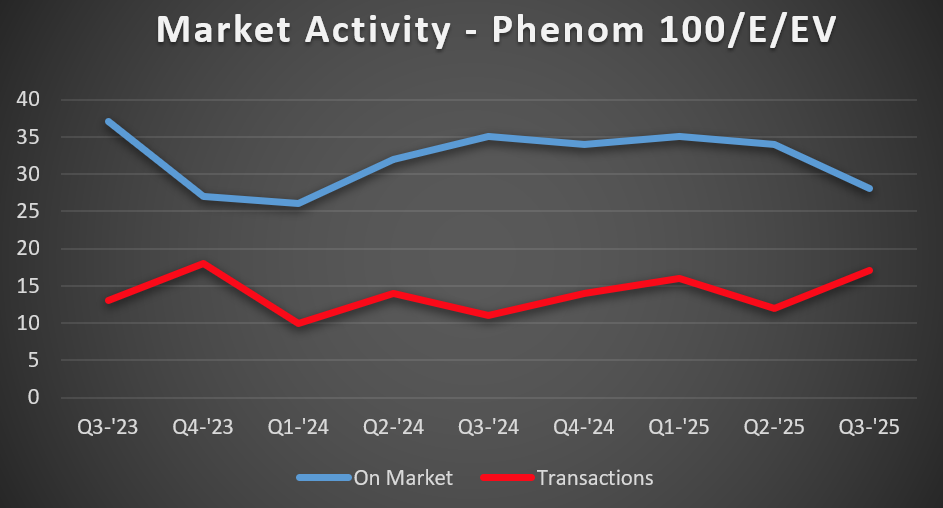

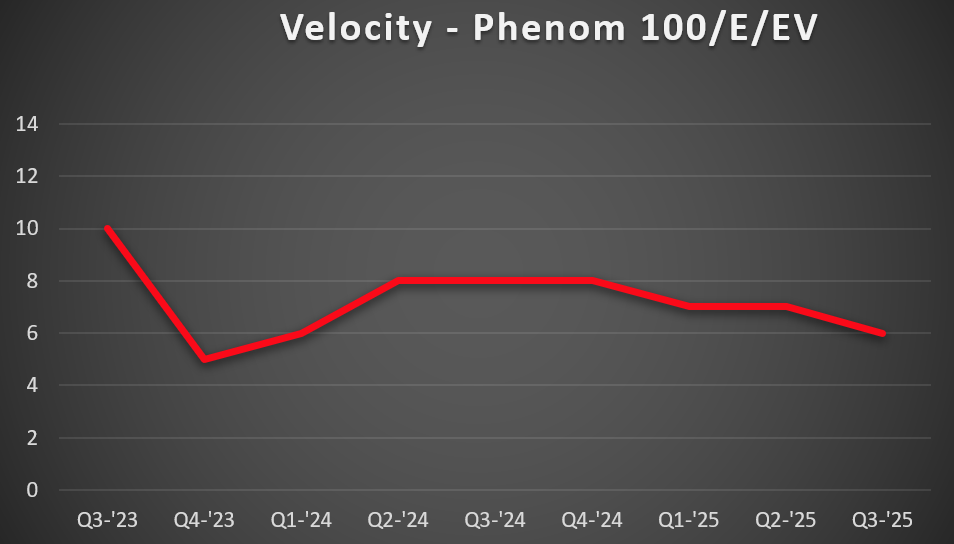

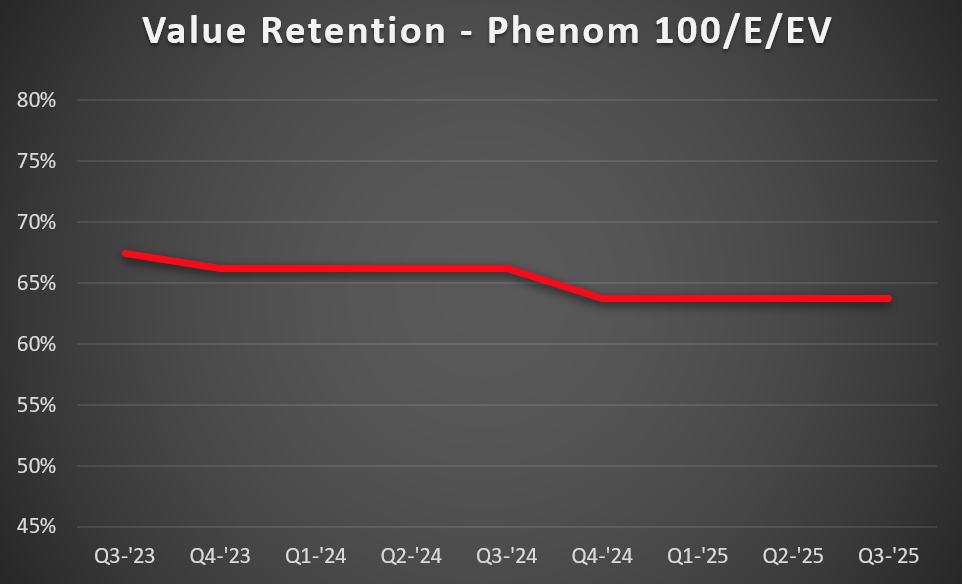

For four consecutive quarters, pricing in the Phenom 100 market remained steadfast. The average number of available aircraft decreased by six, while the number of transactions increased by 41% from Q2 2025 to Q3 2025. Today, the Phenom 100 market is one of the most stable and consistent aircraft markets. Buying or selling in this market will grant you an opportunity for fair pricing on either side.

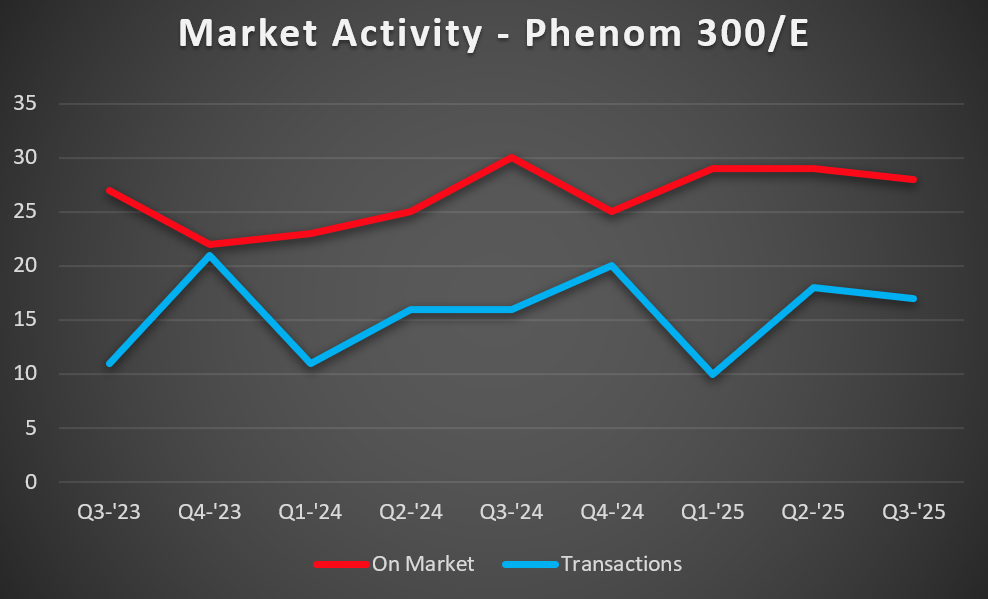

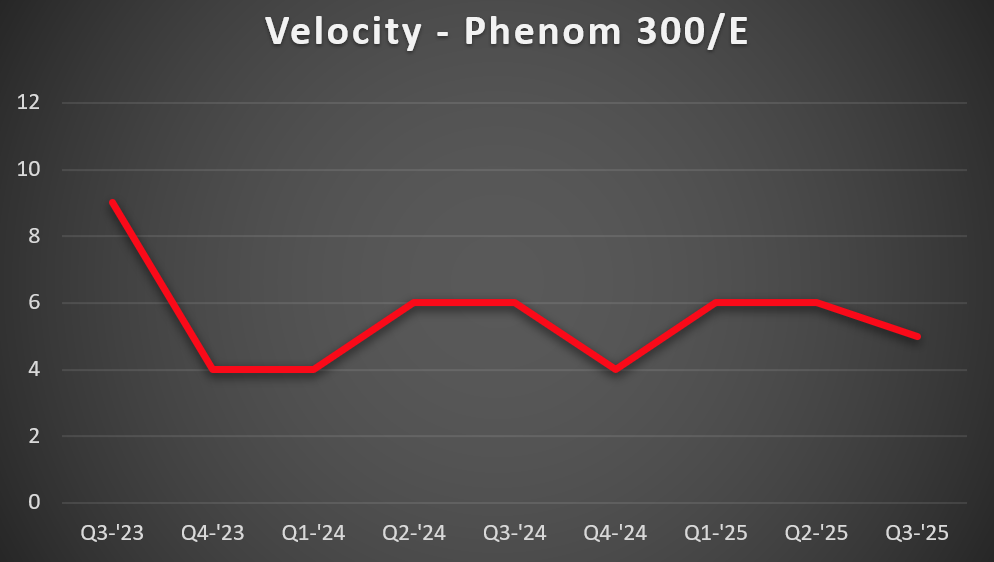

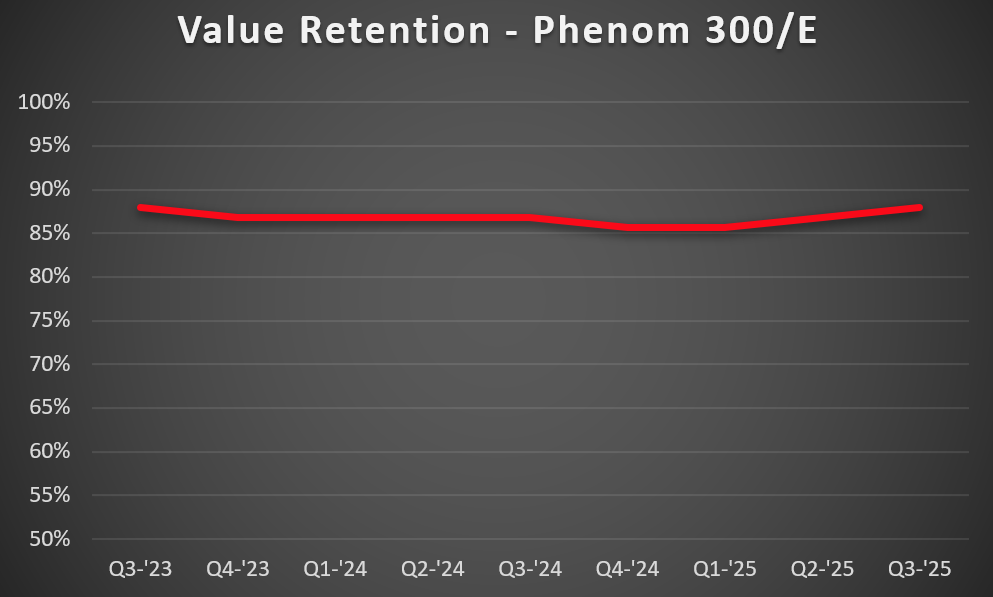

The Phenom 300 continues to be a seller’s market. This aircraft, in fact, remains so in demand that the value of the Phenom 300 has increased by 1% per quarter over the last 2 quarters. Average inventory and transactions remained consistent from Q2 to Q3. This consistency follows through from the increase in transactions by 80% from Q1 to Q2 of 2025. Now is still a great time to sell your Phenom 300/E if you have been on the fence about it.

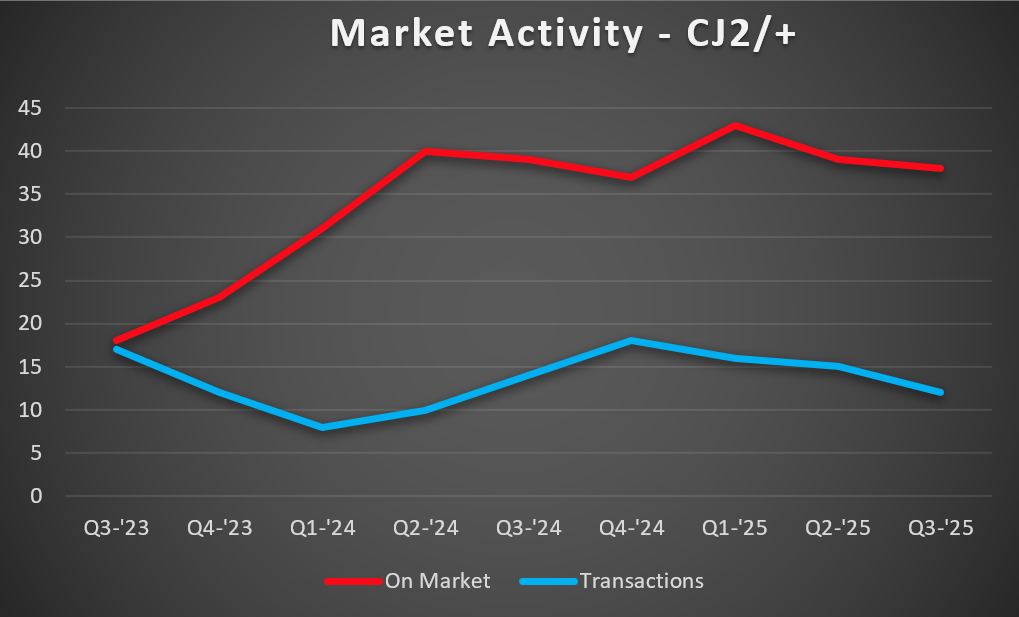

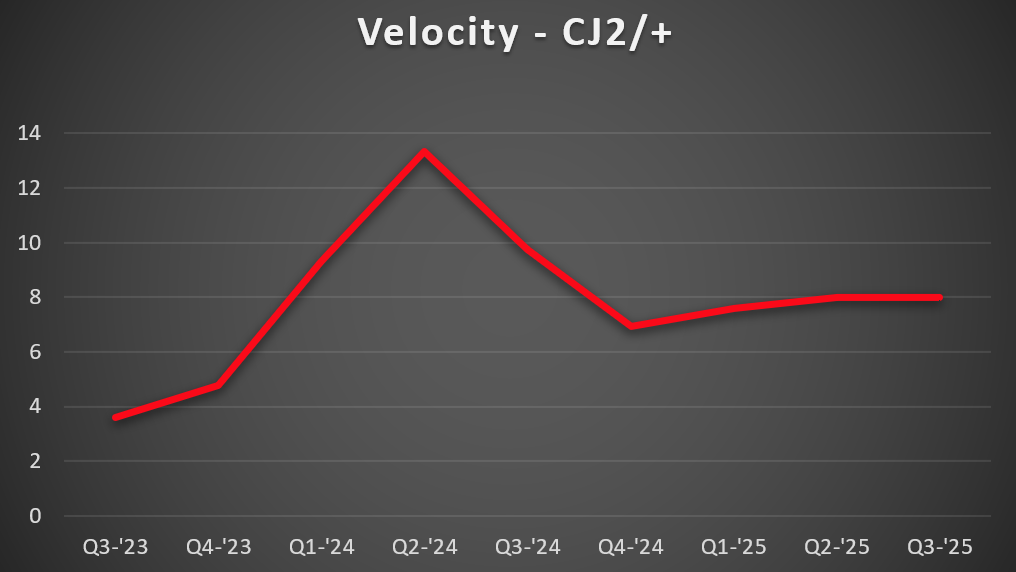

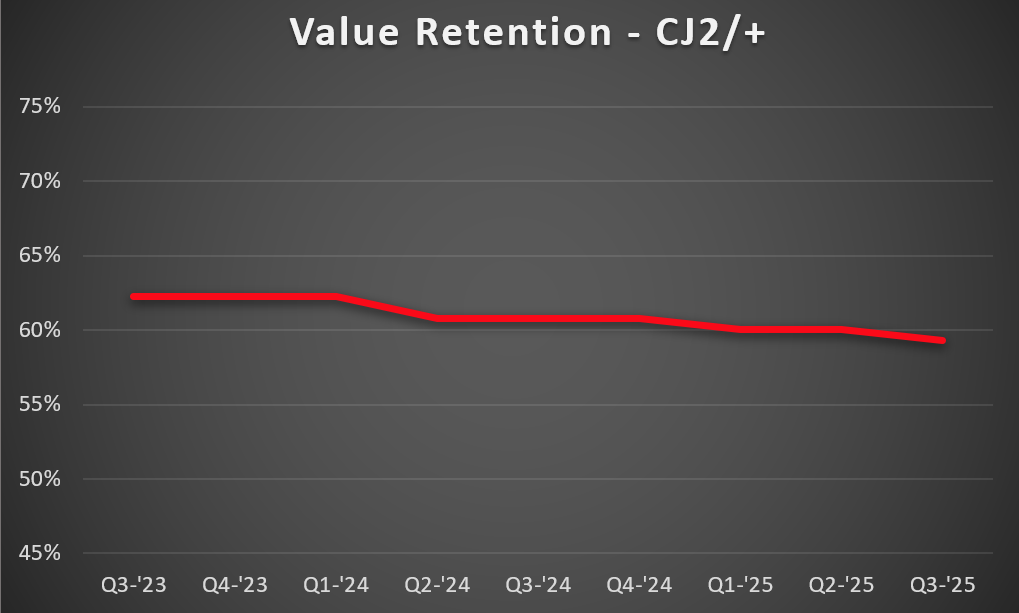

Values for CJ2’s lowered from Q2 to Q3. Average inventory remained relatively stable from 39 in Q2 to 38 in Q3. Transactions continue to drop for the third quarter in a row. However, consistent buying pressure has kept market velocity steady at around eight months for those same 3 quarters. Overall, the CJ2 market is leaning toward a buyer’s market, as values continue to soften and transaction activity declines. However, demand remains resilient for low-time, well-maintained aircraft, giving sellers of premium examples a relative advantage.

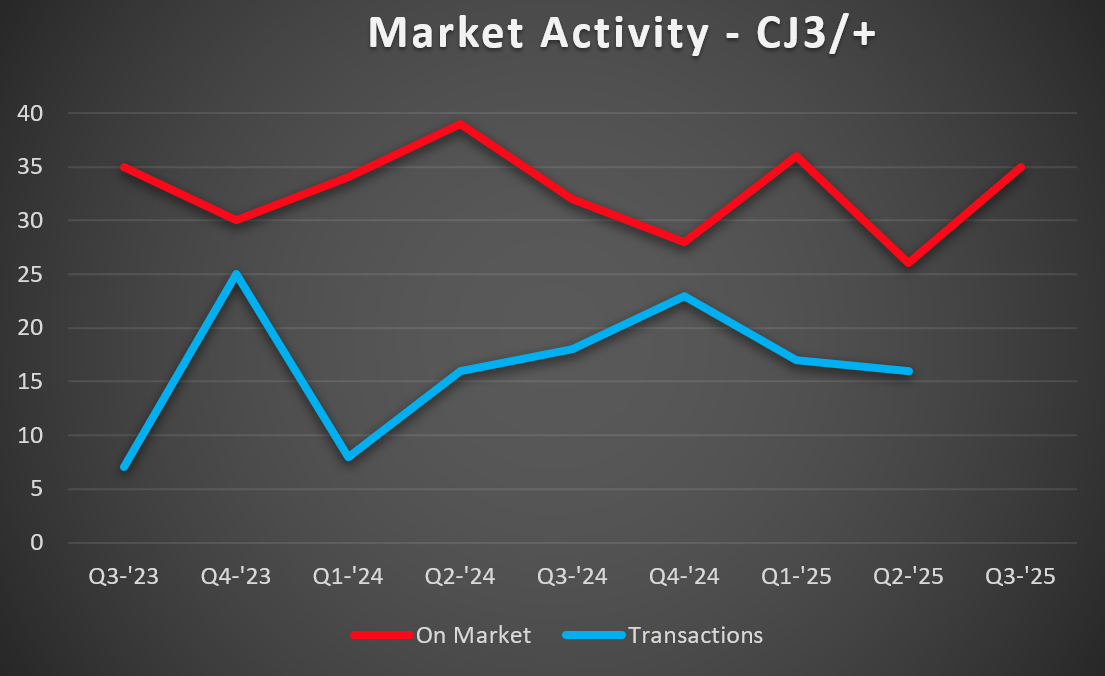

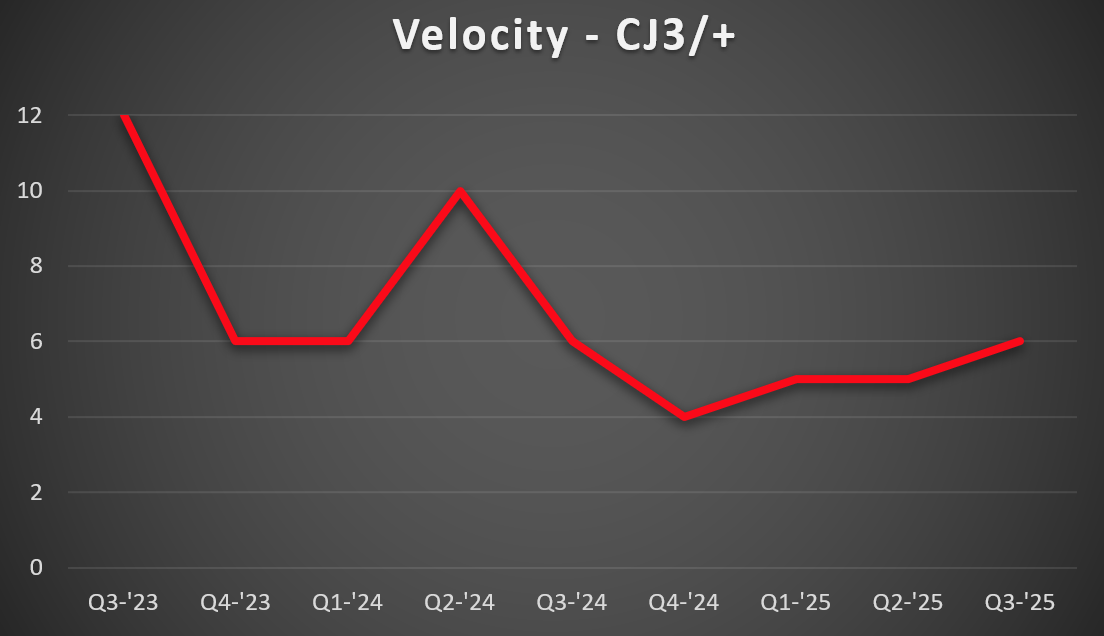

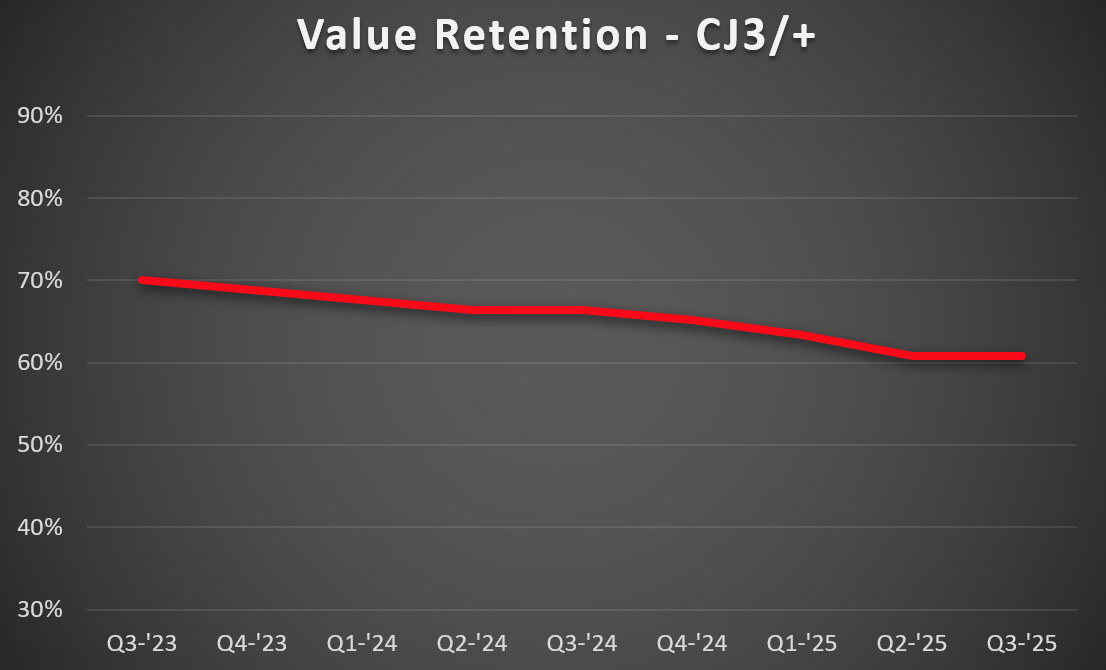

The CJ3 market saw another notable increase in inventory during Q3 2025. Unlike the surge earlier in the year, this round of new listings was not quickly absorbed, leading to a slower market velocity. Despite this, values remained stable from Q2 to Q3, and buyer interest continues to show resilience. Overall, the CJ3 market appears to be balanced but gradually shifting toward a buyer’s market, as growing inventory is beginning to outpace demand, even though underlying buying pressure remains steady.

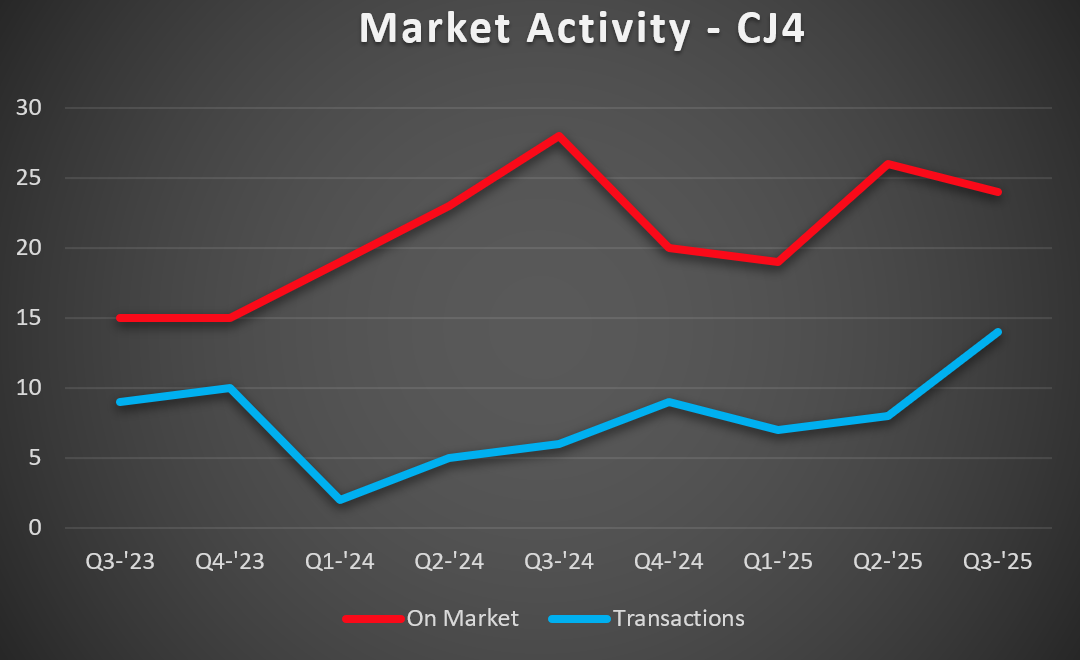

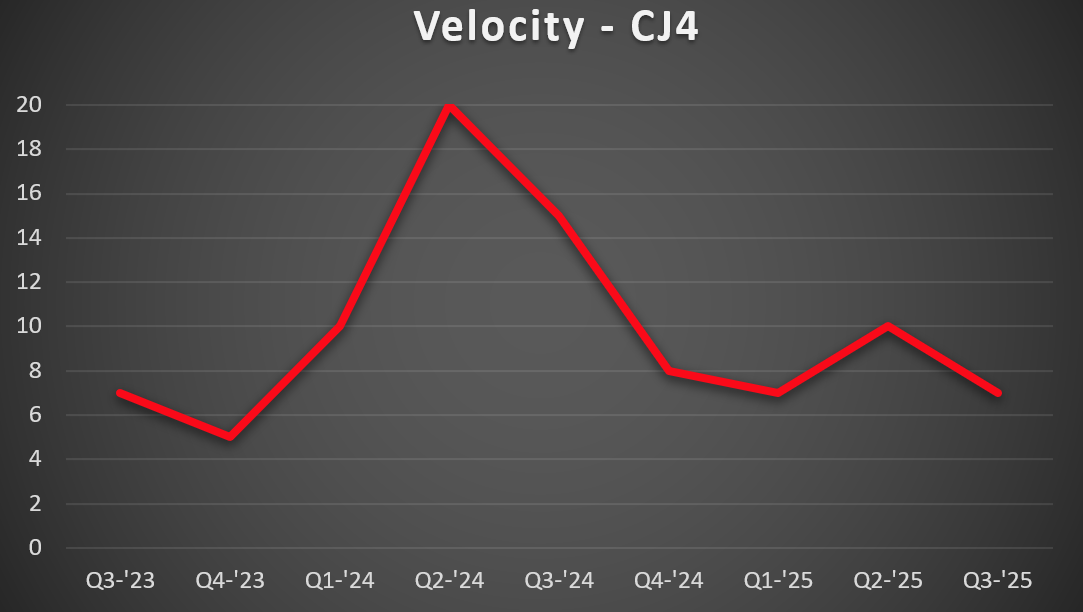

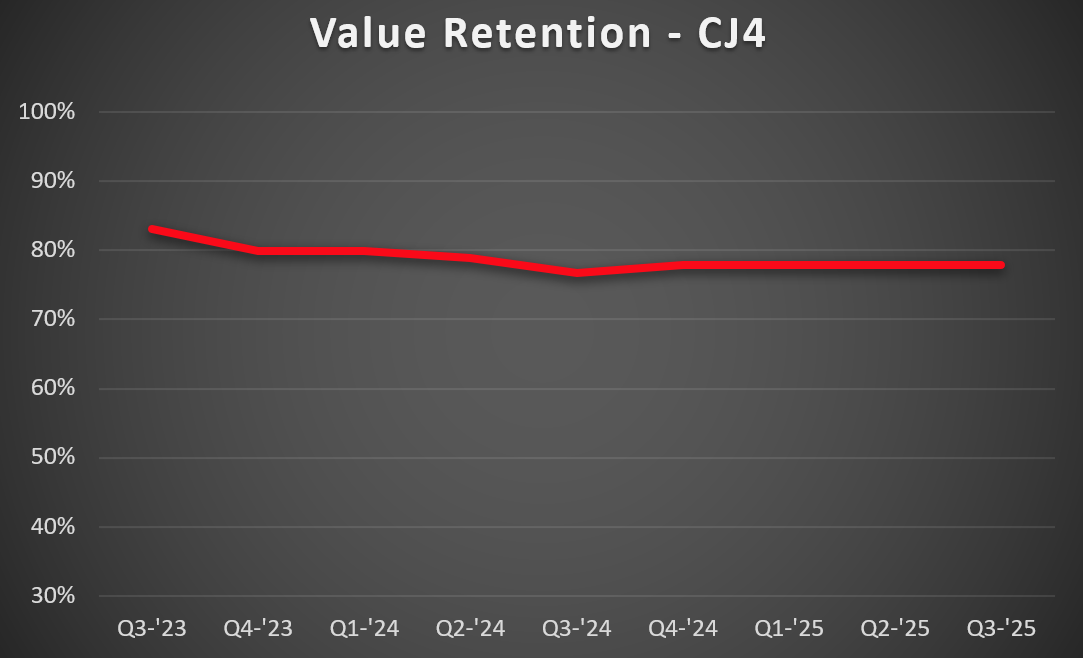

The CJ4 market has maintained stable values over the past four quarters. Transaction activity rose sharply, up 75% from Q2 to Q3, while available inventory declined from an average of 26 to 24 aircraft. These trends reflect strengthening demand and tightening supply, indicating that the CJ4 market is currently leaning toward a seller’s market. Sellers are strongly encouraged to complete the window corrosion service bulletin—or at least have it scheduled—prior to listing their aircraft, as market preference continues to favor CJ4s that have complied with this SB.

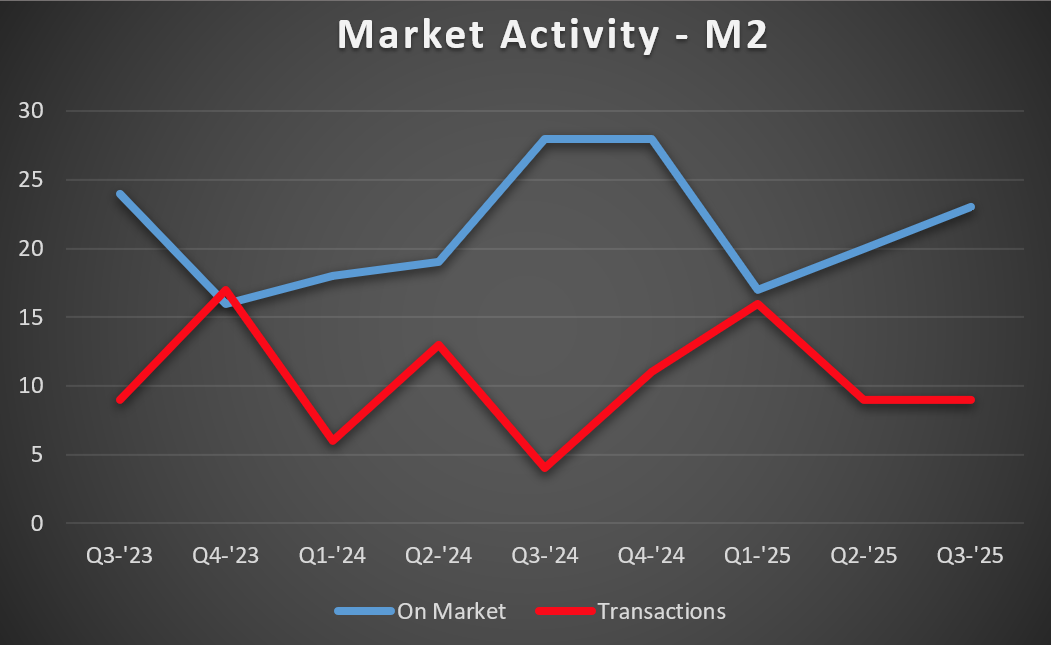

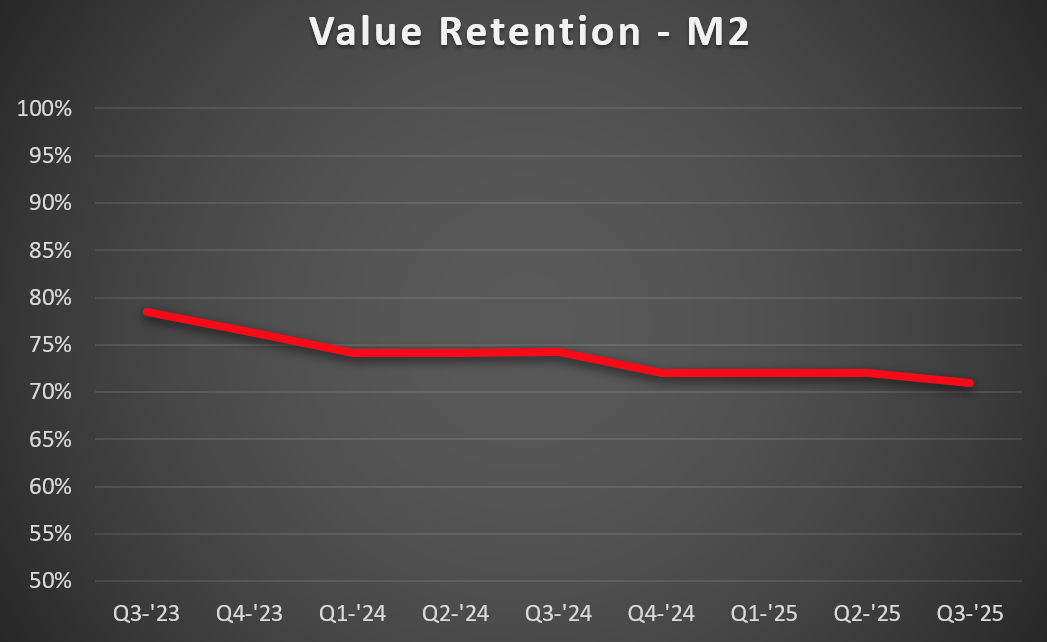

While still a popular market, the Citation M2 continues to show a slight slowdown in overall activity. Transaction volume held steady from Q2 to Q3 2025, following a sharp 70% decline from Q1 to Q2. Meanwhile, available inventory has continued to rise, increasing from 20 aircraft in Q2 to 23 in Q3. Values have softened marginally, down about 1% over the last quarter. These trends indicate that the M2 market is gradually shifting toward a buyer’s market, with more options available and pricing showing mild downward pressure.