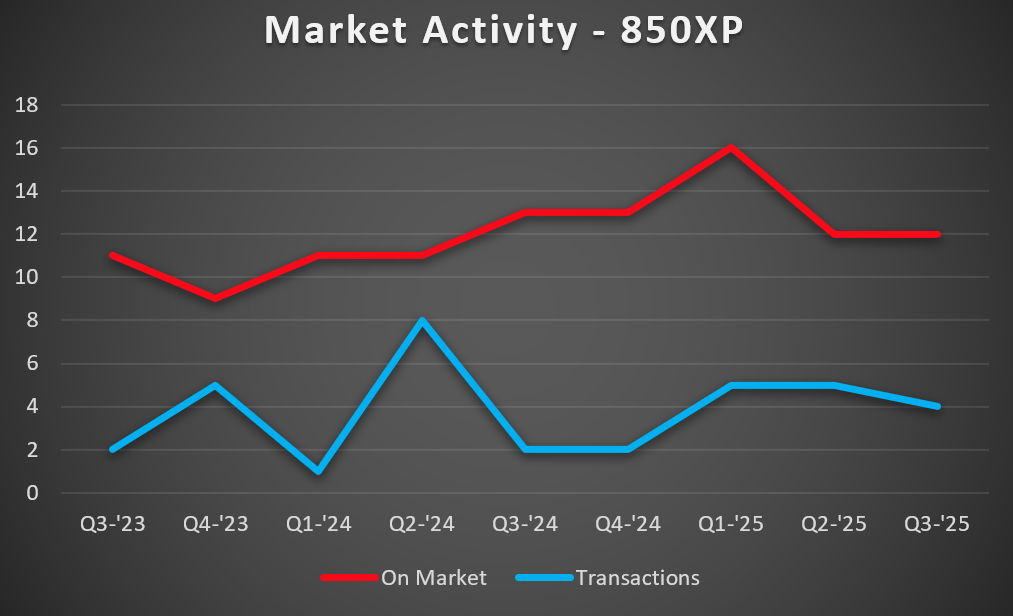

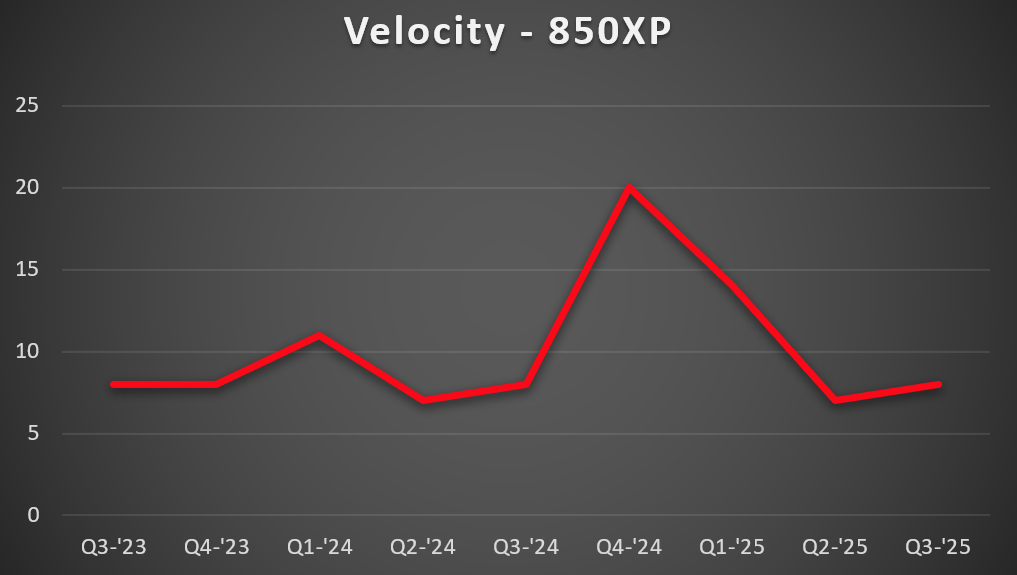

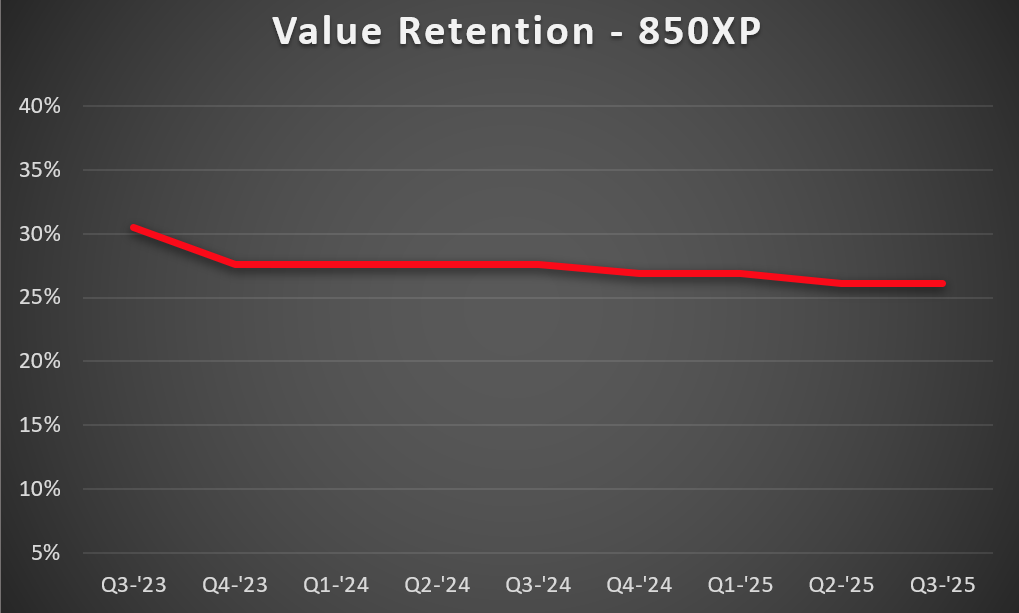

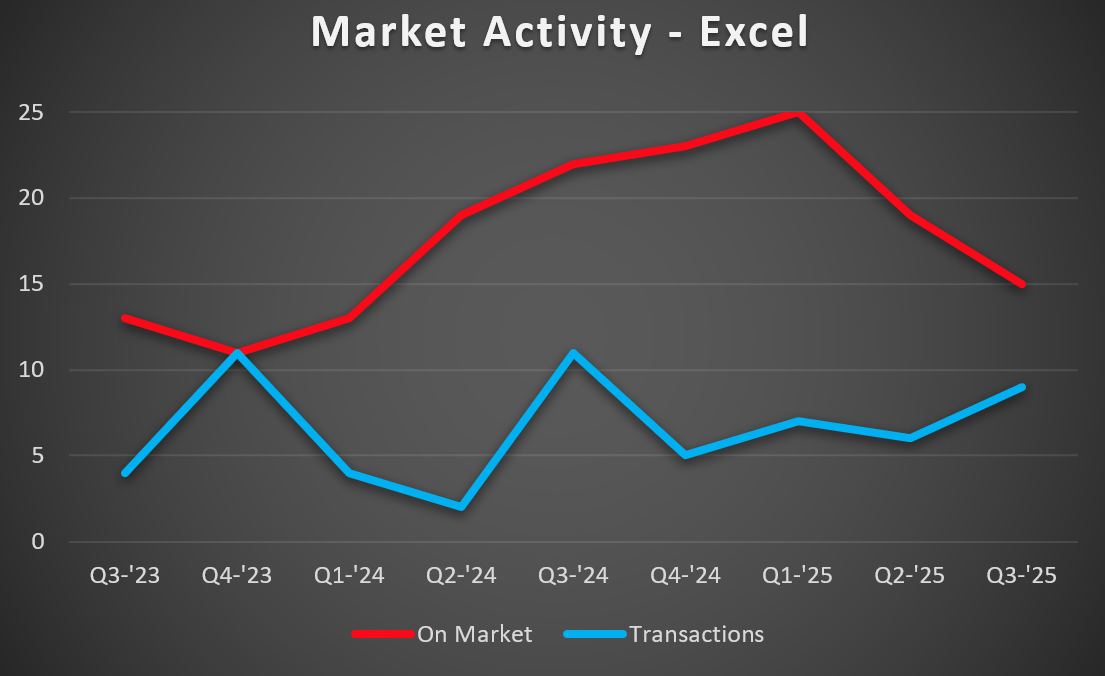

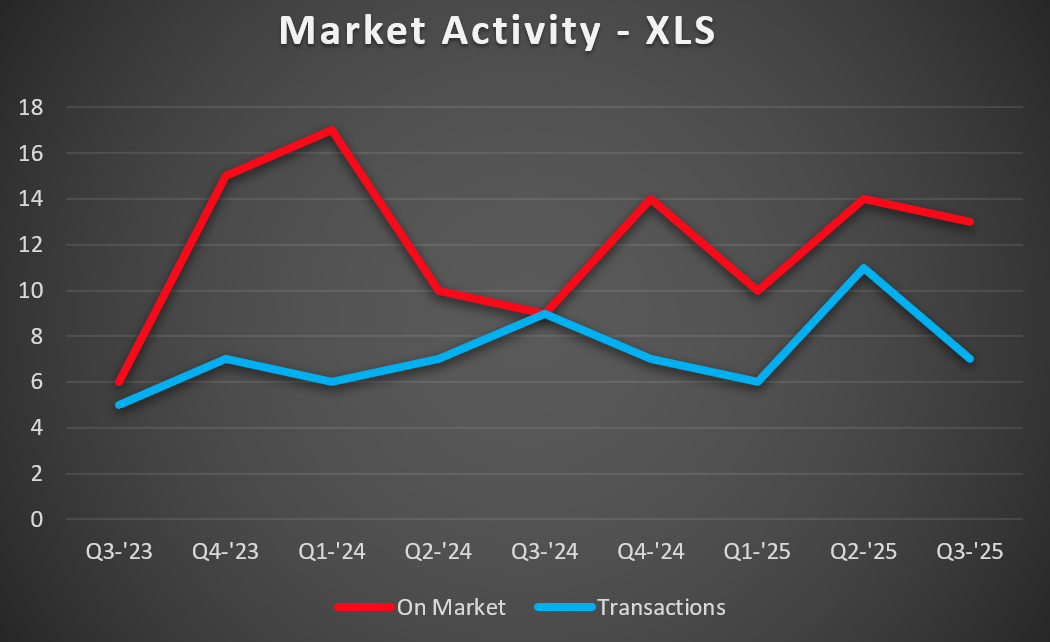

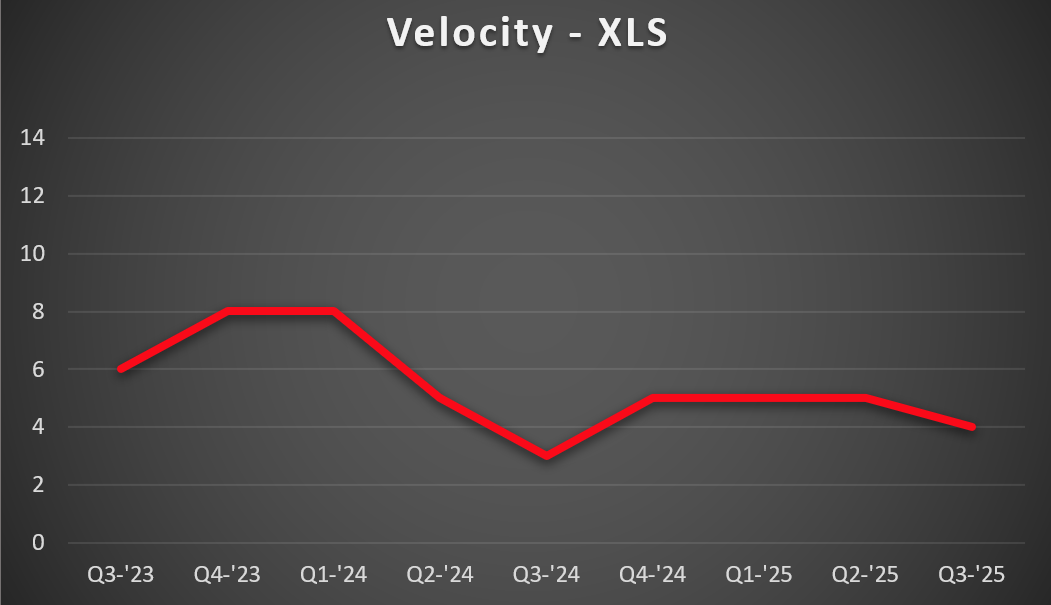

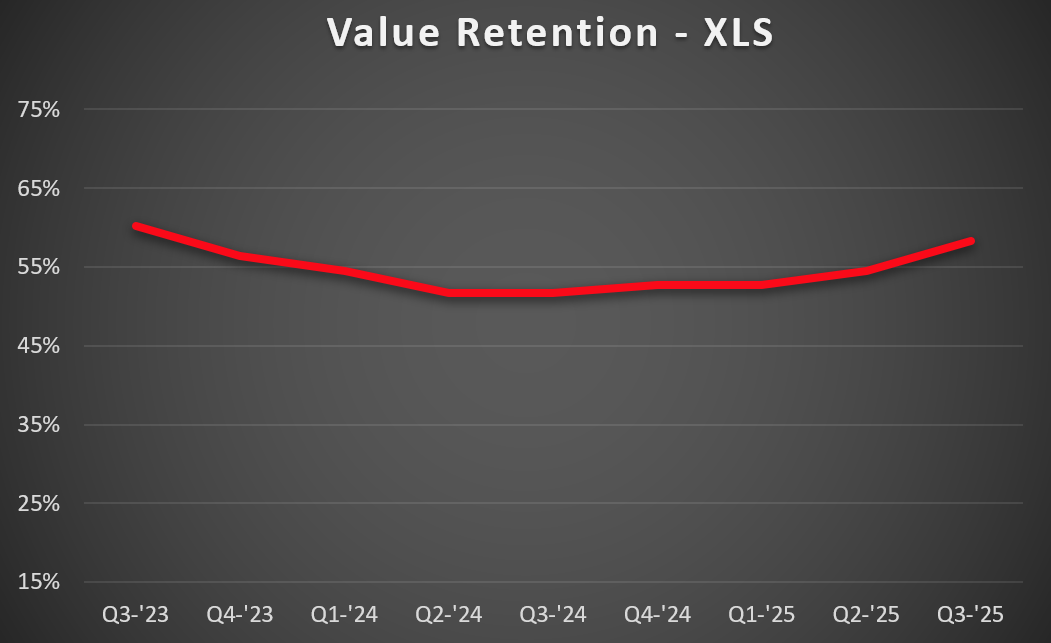

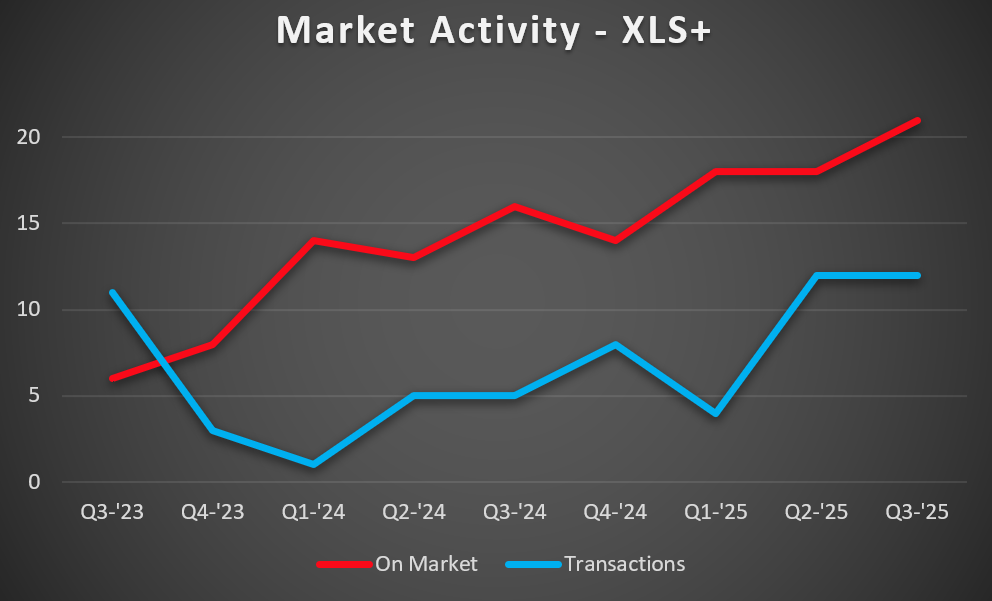

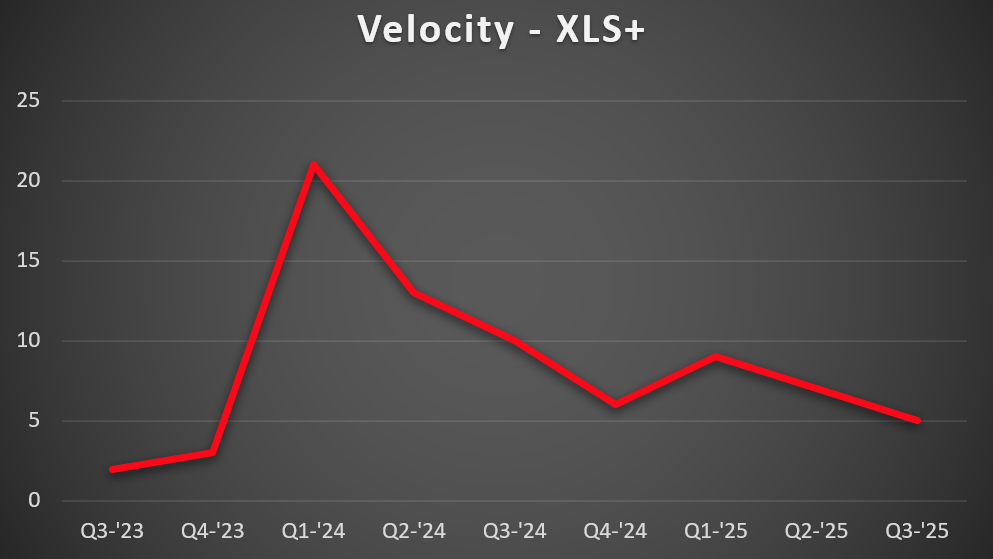

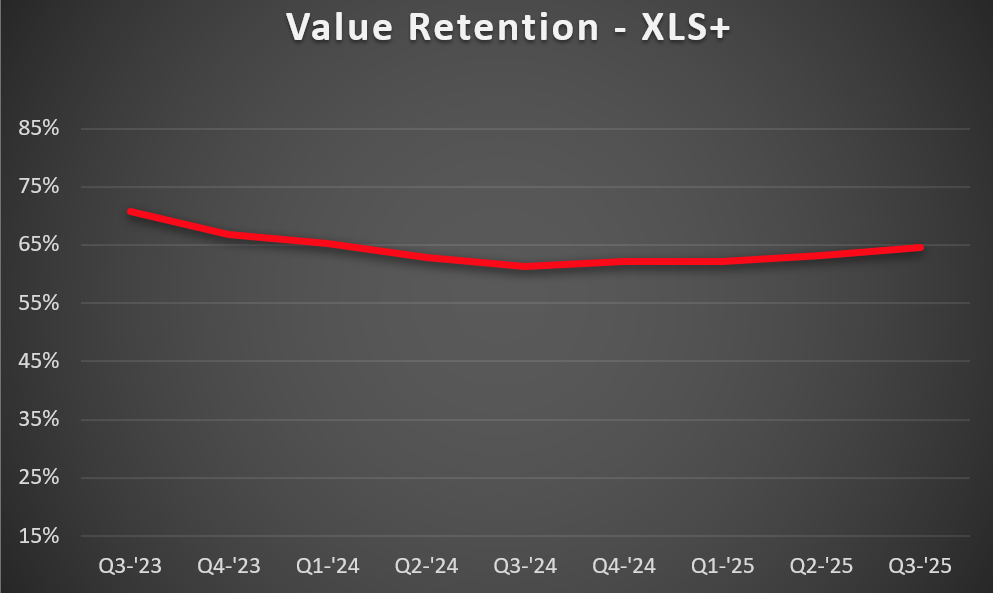

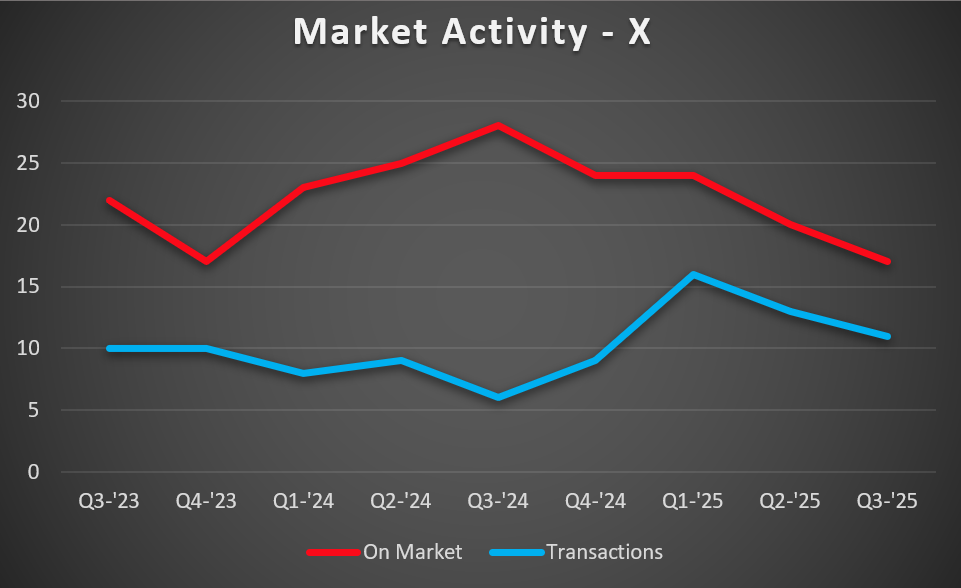

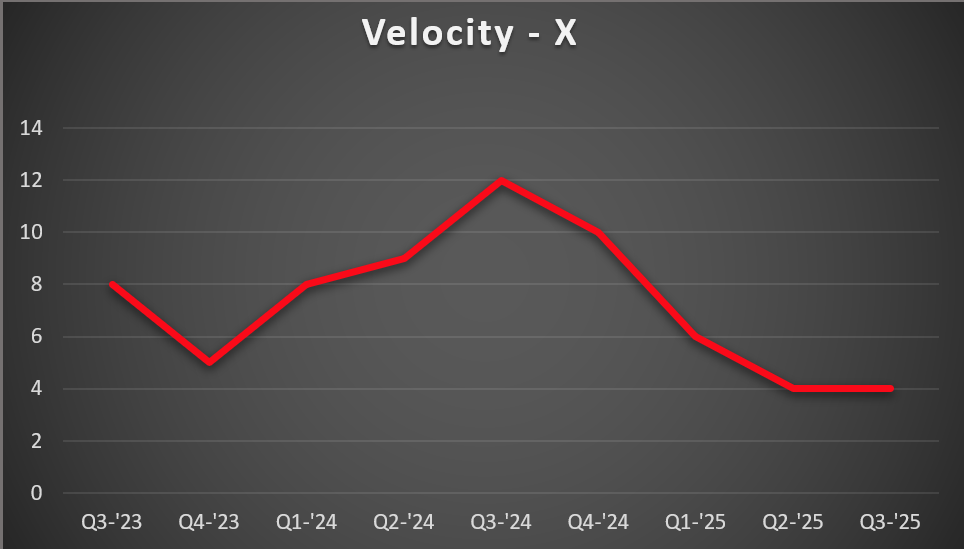

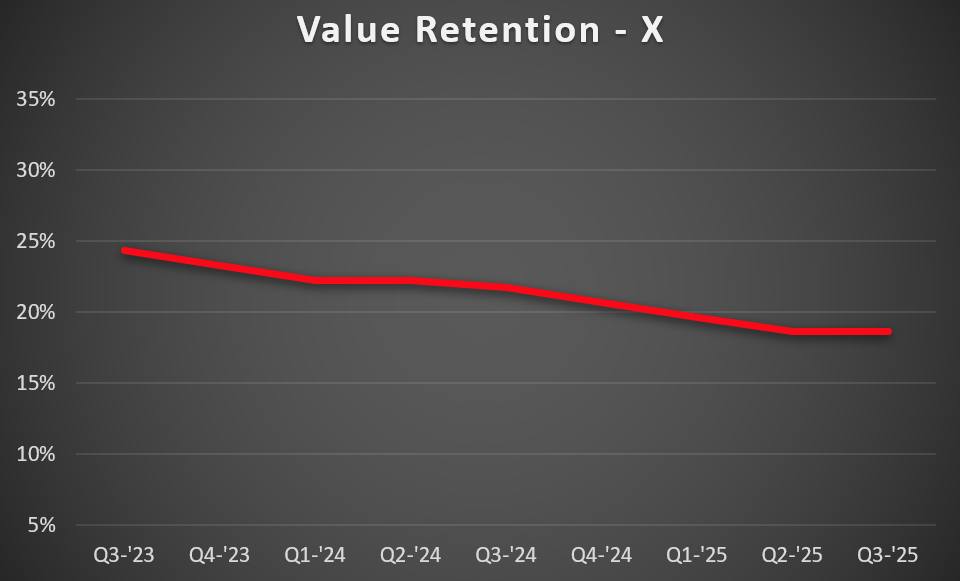

Hawker 850XP inventory, demand, and pricing are all holding steady. There are 12 listings in this market, similar to last quarter, and down four units from Q1. With the first quarter of 2025 being the outlier with elevated inventory, the number of listings in this market has been relatively stable, going back all the way to Q1 of 2024. Demand remains consistent, with four sales taking place during Q3. This makes 14 total transactions on the year, ahead of 2024’s pace of 11 sales by this time. Pricing is holding steady, as this market seems to have found its footing a little closer to 900XP values than in previous years. With steady inventory and pricing, this market remains balanced for buyers and sellers.